We’ve been busy the past few weeks. First, we announced we would be bringing Apple Pay to Italy, and shortly after we announced we would bring it to Spain. Our customers in France started to raise some eyebrows. Our comments section was flooded with questions and requests, as it always is, which is why we’re excited to break the next piece of news.

Later this year, N26 will bring Apple Pay, which is transforming mobile payments with an easy, secure and private way to pay that’s fast and convenient, to customers in France. N26 is proud to bring Apple Pay to France. Supporting Apple Pay is another example of the innovation for which N26 is so well known.

Philippe J DEWOST's insight:

Another reason to consider N26 as one of the best #neobanks out there...

Apple Inc. is in discussions with US banks to develop a mobile-to-mobile payment service that would let users transfer money to one another from their phones, which seems to be something very similar to Venmo and PayPal.

Apple’s own payments system Apple Pay along with other mobile payment systems has been focusing on moving customers away from their wallets, cash, checks and cards in mobile-to-merchant relationships. The new service will be entering the highly competitive space of mobile-to-mobile transactions where PayPal and Venmo have significant shares.

In July, LTP reported that Apple had filed a patent application titled, “Person-to-Person Payments Using Electronic Devices” to the US Patent and Trademark office. Apple has proposed using mobile devices to make payments between persons through various technologies like Wi-Fi, Bluetooth and near-field communication (NFC). Apple filed the patent on September 30, 2014 and credits Apple’s Senior Wireless Software Architect Ahmer A. Khan and Senior Director of Engineering Timothy Hurley for the invention. It got published on July 2, 2015.

What might be really interesting is that from the July patent, it looks like it might have a proximity P2P payment system apart from remote capabilities. It actually talks about the process in which a user will launch a Passbook or wallet app, such as Apple Wallet to detect “nearby devices” they want to send payments to and plug in whatever amount they want to send. The payment would then be authenticated by multiple procedures.

Philippe J DEWOST's insight:

Apple’s CEO Tim Cook recently gave a speech in Trinity College in Dublin, where he shared his insights on the way digital payments will conquer the space,saying, “Your kids will not know what money is.”

The animal kingdom contains numerous examples of individuals cooperating with one another to achieve impressive outcomes without the need for planning, control, or even direct communication between agents – examples are bees, ants, and schools of fish. Humans, however, have only been able to achieve goals cooperatively through the imposition of organizational hierarchies, centralized coordination, and rules.

Blockchain technologies offer a new approach, allowing us to achieve large-scale and systematic cooperation in an entirely distributed and decentralized manner. The application of this technology, however, has mostly focused on transaction-driven financial models like Bitcoin, but the Blockchain’s ability to transact and cooperate on a peer-to-peer basis, without relying on any centralized authority or middlemen, has many other applications. The Blockchain offers a new governance model with implications well beyond financial markets.

Primavera De Filippi is a permanent researcher at the National Center of Scientific Research (CNRS) in Paris. She is currently a research fellow at the Berkman Center for Internet & Society at Harvard Law School, where she’s investigating the concept of governance-by-design as it relates to distributed online architectures. Most of her research focuses on the legal challenges raised, and faced by emergent decentralized technologies – such as Bitcoin, Ethereum and other blockchain-based applications – and how these technologies could be used to design new governance models capable of supporting large-scale decentralized collaboration and more participatory decision-making.

Philippe J DEWOST's insight:

Must see enjoyable and remarkable TEDx talk with a nice approach to the blockchain topic.

Une question revient souvent dans les débats sur le bitcoin : « quelle est l’autorité centrale qui le gère ? » La réponse, connue même si elle n’est pas toujours bien comprise, est : « il n’y en a pas, c’est un réseau pair à pair décentralisé et les règles de gestion sont inscrites dans le code ».

Pour beaucoup, cette réponse ne fait que déplacer le problème : « quelle est alors l’autorité centrale qui gère le code ? » demandent-ils. La réponse à cette deuxième question est beaucoup moins connue : « Il n’y en a pas non plus, les règles d’évolution du code sont elles aussi inscrites dans le code ».

L’explication nécessite un assez long détour par la technique, notamment par le protocole de construction de la « blockchain », qui est très mal connu bien qu’il forme le véritable cœur du système. Pour beaucoup, cette opération se résume à la constitution des « blocs » de transactions, alors que la phase suivante d’assemblage des blocs, qui est encore plus vitale pour la sécurité du système, est largement ignorée. Comme si on réduisait la construction de la Tour Eiffel à la fabrication de ses éléments dans les ateliers de Levallois, en ignorant son montage sur le Champ de Mars. C’est donc à cette deuxième phase que le présent article est consacré.

A cette question simple, la réponse est encore plus simple : personne ! Enfin, pas complètement... Et c'est là que ça se complique. Le processus est quand même très contre-intuitif. Merci à Jacques Favier qui nous a suggéré cet article, particulièrement bien aligné sur la thématique du consensus décentralisé, fil rouge de la session 2015/2016 du CHECy.

Aurez-vous encore votre liberté lorsqu'il faudra choisir entre payer cher sa mutuelle santé, ou accepter de voir son comportement scruté par des machines au service de l'assurance ? Pour le moment sous forme d'un jeu donnant droit jusqu'à 100 euros de médecine douce, AXA montre l'avenir de l'assurance santé liée aux objets connectés et à la médecine personnalisée...

Philippe J DEWOST's insight:

Article à mon avis un peu biaisé ex ante, et qui a mon sens omet deux enjeux que sont : la fidélité de la mesure (j'aimerais savoir de combien un Pulse, un FitBit, et une appli comme Moves divergent en moyenne) d'une part, et l'intégration de ces mesures ou non dans le champ de l'hébergement des données de santé.

LoopPay, the mobile wallet that transmits payment data to magnetic stripe payment card readers, will today announce an Android version of its payment app, which launched on iOS in February. “This is just another step, and we’re taking many steps toward getting more Loop-ready solutions out there,” LoopPay CEO Will Graylin tells us. Currently available as a $39 key fob that pairs with the app, Loop uses a magnetic coil to transmit payment card data. Users simply hold up the fob to a merchant's card reader in order to pay. Soon, a LoopPay iPhone 5/5s charge case will be available, and the company is hoping to convince manufacturers to build Loop’s transmitter into handsets. Still in its early stages, the company numbers its users in the thousands — but Graylin stresses LoopPay's advantage in that virtually all merchants are already equipped to accept LoopPay-powered transactions.

From 29 April you can use your mobile to make person-to-person payments. As phones with debit-card style chips are planned, cash, plastic, even wallets could be redundant

This is a VERY good summary by the Guardian of the next roll outs for mobile payments by banks and telcos in the UK. If implemented correctly, it means that : p2p payments through mobile phones will be free (for individuals) and handled by banks. If you don't live in the UK, there is a payment system called Faster Payment (free, allows almost immediate transfer from person to person, usually online/phone) which is very widely used/

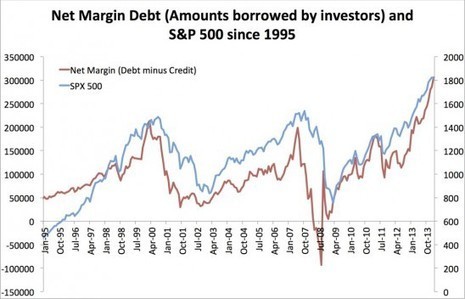

After he left Tamale, Fawcett started spending time with quantitative traders (i.e., quants) and the more he learned about how they created trading algorithms, the bigger and bolder his next idea became. The outcome of his thinking led him to a pivotal insight: the time had come to disrupt the exclusive world of quantitative hedge funds. How would he do it? By harnessing the power of crowdsourcing to build a community of quants, feeding that community with lots of data and incentivizing the community (through regular contests and events) to produce new strategies that could be used in live trading. Today, that unique approach has been transformed into one of the mostly closely watched fintech companies in America. For the company’s next act, Fawcett and his co-founder, Jean Bredeche, are hard at work in laying the foundation to launch an in-house hedge fund utilizing strategies generated from its 100,000+ member community. The FR’s Gregg Schoenberg recently sat down with Fawcett to learn more about his company and the bold moves he’s making to level the playing field in one of the most lucrative — and heretofore undisrupted — corners of the investment management universe.

Philippe J DEWOST's insight:

When Quantitative Trading mingles with the Crowd. Will 2017 see the advent of new types of investment funds backed with thousands of LPs ?

The Ethereum project and ConsenSys, the company created by one of the project’s co-creators, have received a huge vote of approval from one of the world’s biggest enterprise software providers — Microsoft. The company will be working with ConsenSys to provide developmenttools for Microsoft’s enterprise customers on the Azure platform.

Focusing on financial services we saw a lot of potential for a framework and platform like Ethereum to go across the platform of financial institutions and modernize a lot of processes that were stuck in the past,” says Marley Gray, Director of Technology Strategy, US Financial Services at Microsoft. “We thought that Ethereum was a really good platform for building distributed ledger applications.”

Unlike bitcoin-based blockchain applications (and companies like Chain that are developing projects on top of bitcoin) Ethereum uses a different token called the Ether.

“Bitcoin offers one functionality which is the monetary functionality. Because it’s a very narrow protocol… it’s difficult to build arbitrarily difficult functionality into the program,” says Joseph Lubin, the founder of ConsenSys, and a major supporter of the Ethereum Foundation.

With Ethereum, there’s a complete computational machine running within every node of the network, Lubin says.

Philippe J DEWOST's insight:

Fragmentation or evolution ? Microsoft's move is interesting anyway and confirms the advent of decentralized consensus as a generic and scalable disruption factor.

To process a transaction, you need first to make sure the sender owns the asset he wants to transfer, and make sure he will not trade it twice.

In the blockchain, information is stored in blocks that record all transactions ever done through the network. Hence, it allows validating both the existence of assets to be traded and ownership.

To avoid double spending, the technology requests several nodes to agree on a transaction to process it. A validation is also artificially difficult to achieve: miners leverage computer power to solve complex cryptographic problems (the proof-of-work). Every time a problem is cracked, a block is added to the chain, and all the transactions it includes are thus validated. The updated chain, including the new block, is shared with other nodes and becomes the new reference; this process leverages cryptography to prevent duplicate transactions.

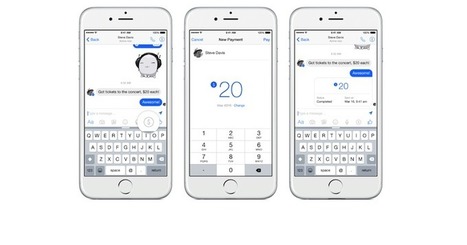

Mobile payment transactions may not be the standard yet but there are a lot of people who prefer this method simply because of its ease and convenience. Others are simply worried about privacy and security but developers like Facebook know how to make an app secure all the time. Frequent updates and releases make sure the app is always in tip-top shape.

The latest update to Facebook Messenger brings a new feature that allows person-to-person (P2P) mobile payments. The P2P payment on Facebook Messenger only requires a debit card or credit card (Visa or Mastercard) so you can send money right away to a contact. To send an amount, open up a conversation, click on the dollar ($) icon, enter amount when prompted, and then click 'Pay'. Amount will be sent immediately to the other person who will receive the money on his or her own checking account.

Philippe J DEWOST's insight:

Messaging apps are the cornerstone of mobile P2P as evidenced by this Facebook smart move.

The credit card companies themselves aren't going anywhere for now. Visa and MasterCard in particular will remain an indispensable part of the chain because they don't actually process payments. They simply provide the rails that the credit card system runs on. Credit card processors like First Data that actually do the work of processing merchants' credit card transactions on the back-end are also in a strong position.Two pieces in the chain are particularly vulnerable to disruption: the makers of the actual hardware — basically card readers and registers — that are used to physically accept card payments at stores, and the hundreds of vendors known as merchant service providers, or MSPs, which set businesses up to accept credit cards.Manufacturers of register systems are vulnerable: Point-of-sale hardware faces an immediate threat from mobile devices. These devices are cheap and easy to implement, they do not require consumers to adopt new behaviors, and they free up retailer space previously devoted to bulky hardware.In addition, the new payments companies — including PayPal, Leaf, Revel Systems, Square, and others — could shove traditional MSPs aside as they bridge the offline and online worlds. They pair their mobile registers with consumer-side smartphone apps, and often also provide additional merchant services, like software for loyalty programs or for parsing online consumer data. These new companies want to replace the old players that focused mainly on logistics, i.e., helping merchants take credit card payments.But it's not all doom and gloom yet for legacy MSPs: they have existing relationships with the majority of merchants who accept credit cards and with banks. They also have established marketing channels and large sales forces. Large MSPs will move to acquire new payments technologies to squelch the disruption threat.

Philippe J DEWOST's insight:

In Tel-Aviv, I paid a taxi with my and his smartphone and a square like dongle. Since, I'm getting more and more interested in #Fintech disruption...

"Banking as we know it is in the midst of enormous change and innovation. We have jumped in by investing in alternative payment models and also by accepting bitcoin for tickets on Virgin Galactic, the world’s first commercial spaceline.

Bitpay has proven itself to process bitcoin safely and reliably, growing the market and increasing adoption, which continues to build trust, legitimacy and momentum in this exciting currency revolution."

To get content containing either thought or leadership enter:

To get content containing both thought and leadership enter:

To get content containing the expression thought leadership enter:

You can enter several keywords and you can refine them whenever you want. Our suggestion engine uses more signals but entering a few keywords here will rapidly give you great content to curate.

Your new post is loading...

Your new post is loading...

Another reason to consider N26 as one of the best #neobanks out there...